"We'll Figure Out the Insurance Later" Is One of the Most Expensive Decisions a Business Owner Can Make

There's a phrase that comes up in nearly every conversation about business succession planning. It shows up at the end of a meeting, after the buy-sell terms have been discussed, after the valuation methodology has been agreed upon, and after the attorneys have drafted an agreement:

"We'll figure out the insurance piece later."

It sounds reasonable. There are a hundred other priorities. The agreement is signed. The plan is in place. The insurance can wait.

But "later" has a cost. And it's usually far larger than business owners expect.

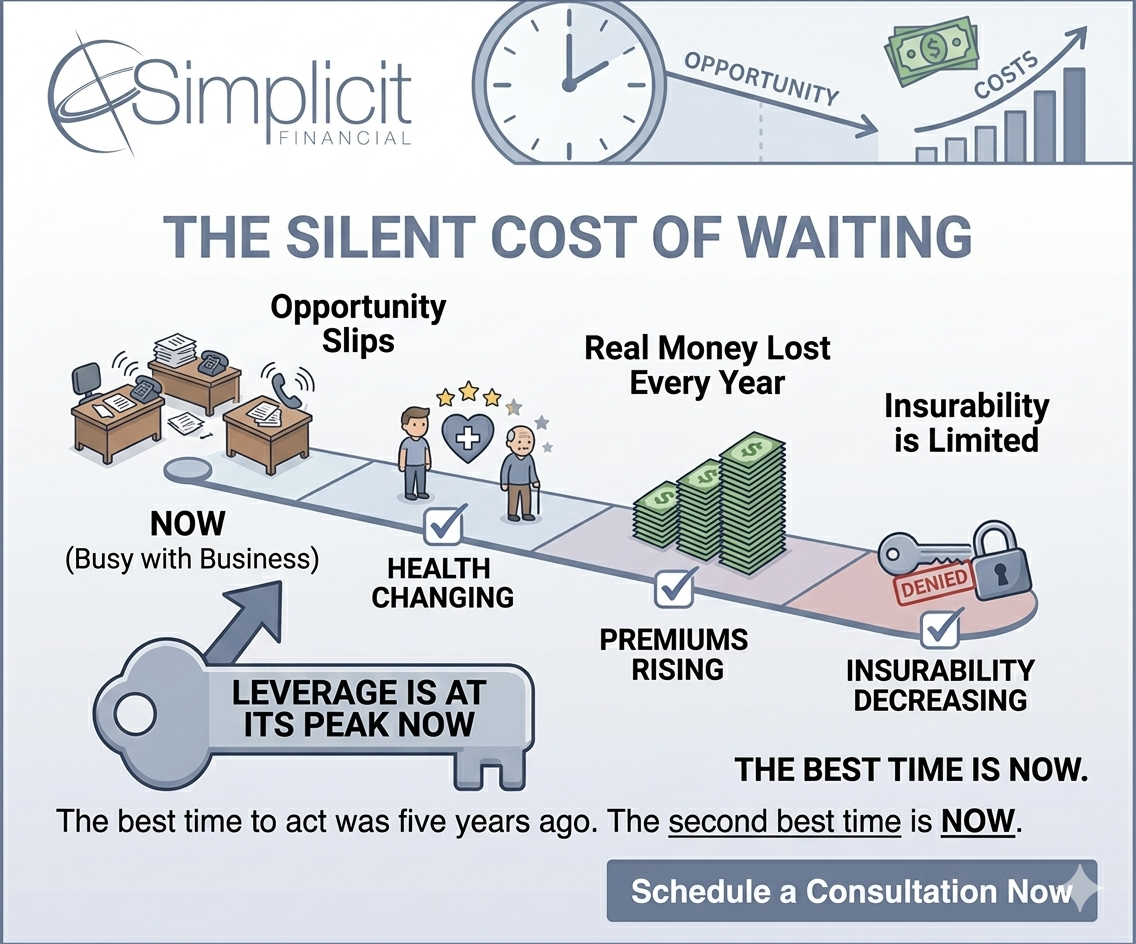

What Changes When You Wait

Life insurance premiums are determined primarily by two factors: age and health. Both work against you over time.

Age is a constant — every year you wait, every policy you could purchase costs more. The premium difference between a 45-year-old and a 55-year-old purchasing the same coverage can be substantial. Multiply that difference across a 20-year policy, and the accumulated cost of waiting becomes a significant dollar figure.

Health is less predictable — and that's exactly the problem. A business owner who delays purchasing coverage and then develops a health condition may face dramatically higher premiums, policy exclusions, or in some cases, complete uninsurability. At that point, the option to fund the obligation through life insurance may no longer exist.

The Obligation Doesn't Wait

Here's the critical asymmetry: the buy-sell obligation, the estate tax liability, the key person exposure — none of these pause while the owner defers the insurance decision. The business continues to grow in value. The taxable estate continues to expand. The dependency on key individuals doesn't diminish.

A business owner who agrees to a $5 million buy-sell buyout and delays insurance by five years hasn't saved five years of premiums. They've left a $5 million obligation completely unfunded for five years — during which any number of triggering events could have occurred.

"The business doesn't stop being valuable while you wait. The estate doesn't stop growing. Only the funding stays at zero."

What Properly Timed Coverage Actually Buys

Purchasing coverage at the right time — when the owner is young and healthy — does several things simultaneously:

Locks in the lowest possible premium rate for the life of the policy

Secures insurability before any health changes occur

Allows cash value to accumulate over time, adding a balance sheet asset to the business or the estate

Funds the obligation from day one, eliminating the exposure window entirely

The business owner who acts now isn't just paying premiums — they're exchanging predictable, manageable annual costs for certainty. The obligation gets funded. The risk disappears.

The Advisor's Role in This Conversation

One of the most important things a financial advisor, CPA, or estate attorney can do for a business owner client is put a number on the cost of delay. Not in abstract terms — in actual dollars.

What does the premium cost today versus in three years? What's the health risk? What's the exposure value of leaving the obligation unfunded in the interim? Most business owners, when they see this analysis laid out clearly, make a different decision than when the conversation stays abstract.

This is exactly the kind of analysis Simplicit Financial provides. We work with advisors to quantify the cost of inaction and build a case that helps clients make informed decisions — not deferred ones.

Simplicit Financial's Role

At Simplicit Financial, we have no carrier bias and no AUM participation. We design insurance solutions that are driven entirely by what serves the client's plan — which means we can be direct about timing, transparent about cost, and objective about structure.

We also work with physician consultants who support the underwriting process, helping clients secure the best possible ratings and the most favorable premium outcomes. The window to lock in those outcomes is open now. It may not stay open.

Don't let timing become the most expensive decision in your succession plan. Contact Simplicit Financial to start the conversation today.