The Pennies-on-the-Dollar Principle: How Life Insurance Funds Large Business Obligations for a Fraction of Their Cost

Buy-Sell Funding and Succession Planning

Every business owner understands leverage. They use it to acquire property, finance equipment, and grow their company. But very few are using it where it matters most: funding the obligations that will define what happens to their business — and their family — when they’re no longer in the picture.

That’s the gap that properly structured life insurance was built to fill.

The Problem With an Unfunded Buy-Sell Agreement

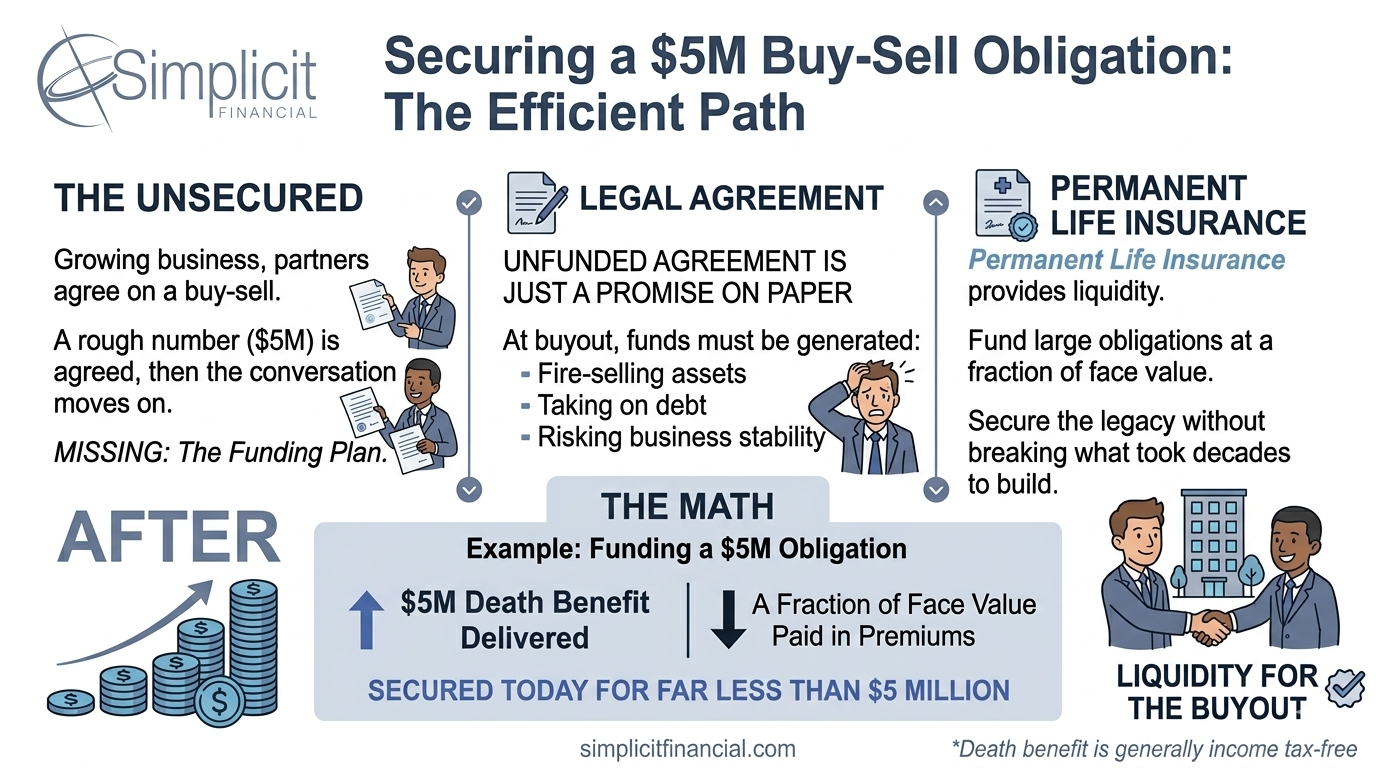

A buy-sell agreement is an essential document. It establishes what happens to a business owner’s interest at death, disability, retirement, or other triggering events. It protects co-owners, protects the business, and creates a clear path forward for everyone involved.

But here’s what’s often missing: the money.

When a triggering event occurs and there’s no dedicated funding mechanism in place, the surviving business partner or the business itself faces an impossible set of options: liquidate business assets, take on debt, negotiate installment buyouts with the deceased owner’s estate, or simply fail to honor the agreement. None of these outcomes are good. All of them were avoidable.

How Life Insurance Changes the Math

Life insurance is a leverage tool. Instead of setting aside $4 million in a savings account to eventually fund a buyout, a business owner pays a premium — a fraction of that obligation — each year. In exchange, the policy delivers the full death benefit at the moment it’s needed.

The Core Principle

Premiums paid over a policy’s life typically represent a small percentage of the total death benefit. A properly structured permanent policy (or Term) may deliver $5M or more in death benefit for significantly less than $5M in total premium outlay. That’s the leverage.

At death, the beneficiary — whether that’s the co-business owner in a cross-purchase structure, or the business itself in an entity redemption — receives the death benefit income tax-free.* Those proceeds are then used to purchase the decedent’s business interest from their estate, as outlined in the buy-sell agreement.

The result: a clean, well-funded transition. The family of the deceased owner receives fair value for the business interest. The surviving partner retains control. The business continues without disruption.

Beyond Death: The Living Benefits of Cash Value

Properly structured permanent life insurance does more than fund a buyout at death. During the policy owner’s lifetime, the cash value accumulates on a tax-deferred basis and can serve multiple functions:

• As collateral or a source of liquidity for the business in an emergency

• As an informal funding vehicle for non-qualified deferred compensation plans

• As a supplemental income source at retirement through tax-advantaged withdrawals and loans

• As a partial down payment in a retirement- or disability-triggered buyout scenario

This is why we consistently say that life insurance in business planning isn’t purely a death benefit product. It’s a living financial asset.

The Structures That Make It Work

How the life insurance is owned and structured matters significantly for both tax purposes and legal compliance. There are multiple Buy-Sell structures; here are three primary ones:

• Cross-Purchase: Each business owner purchases a policy on the life of the other(s). At death, the surviving owner receives the death benefit and uses it to purchase the deceased owner’s interest. This approach was recommended by the Supreme Court in Connelly v. United States as a way to avoid estate tax complications.

• Entity Redemption: The business owns and is beneficiary of the policies on each owner’s life. At death, the business uses the death benefit to redeem the deceased owner’s interest. Post-Connelly, this structure requires careful review to ensure estate tax compliance.

• Wait-and-See: A hybrid approach that preserves flexibility — the business or the co-owners can choose to execute the purchase at the triggering event, depending on circumstances.

Each structure has distinct tax, legal, and liquidity implications. The right choice depends on the number of owners, the size of the estates involved, and the business’s overall succession strategy. This is exactly where an unbiased insurance specialist — working alongside the estate attorney, CPA, and financial advisor — adds irreplaceable value.

The Real Cost of Waiting

Every year that passes without a funded succession plan is a year the business is exposed. Premiums are lower when owners are younger and healthier. The cost of delay isn’t just financial — it’s the risk that one of the owners becomes uninsurable, or worse, that a triggering event occurs before the plan is in place.

Common Objection: “We’ll figure out the insurance later.”

This is one of the most expensive decisions a business owner makes — not because of what they spend, but because of what they lose. Later often means higher premiums, fewer options, or no options at all. The cost of waiting is rarely visible until it’s too late.

What “Properly Structured” Actually Means

Not all life insurance policies are equal, and not all structures serve the same goals. At Simplicit Financial, we work without carrier bias and without AUM participation. That means our recommendations are built entirely around the client’s situation — not a product shelf or a revenue target.

Properly structured means the right death benefit amount tied to the business valuation method in the agreement. It means the ownership and beneficiary designations match the buy-sell structure. It means the premium design supports long-term cash value growth while keeping the death benefit in force. And it means the structure is reviewed and updated as the business grows and ownership changes.

An agreement that was properly designed when the business was worth $2 million may be dramatically underfunded when the business reaches $8 million. Regular reviews matter.

Putting It Together

A funded buy-sell agreement using life insurance is one of the clearest examples of the “pennies on the dollar” principle at work. It’s not a complicated concept — it’s a straightforward application of leverage to a real, quantifiable future obligation.

What’s complicated is getting the structure right. And that’s where most advisors need a specialist at the table.

Ready to review a client’s buy-sell funding?

Simplicit Financial works alongside estate attorneys, CPAs, and investment advisors to evaluate, design, and implement life insurance strategies for business succession planning. No carrier bias. No AUM participation. Just the right solution for the client. Contact us to start the conversation.

* For federal income tax purposes, life insurance death benefits generally pay income tax-free to beneficiaries pursuant to IRC Sec. 101(a)(1). In certain situations, life insurance death benefits may be partially or wholly taxable. Consult your tax advisor for guidance specific to your situation.