Carrier Bias Is Costing Your Clients Money. Here’s What Objective Insurance Advice, A Fiduciary’s Advice, Actually Looks Like.

Carrier Bias Gap

There is a structural problem in the life insurance industry that most business owners and their advisors don’t fully understand — and it’s costing clients real money.

It’s called carrier & product bias. And it affects nearly every insurance recommendation that comes from someone with a carrier relationship.

What Is Carrier or Product Bias?

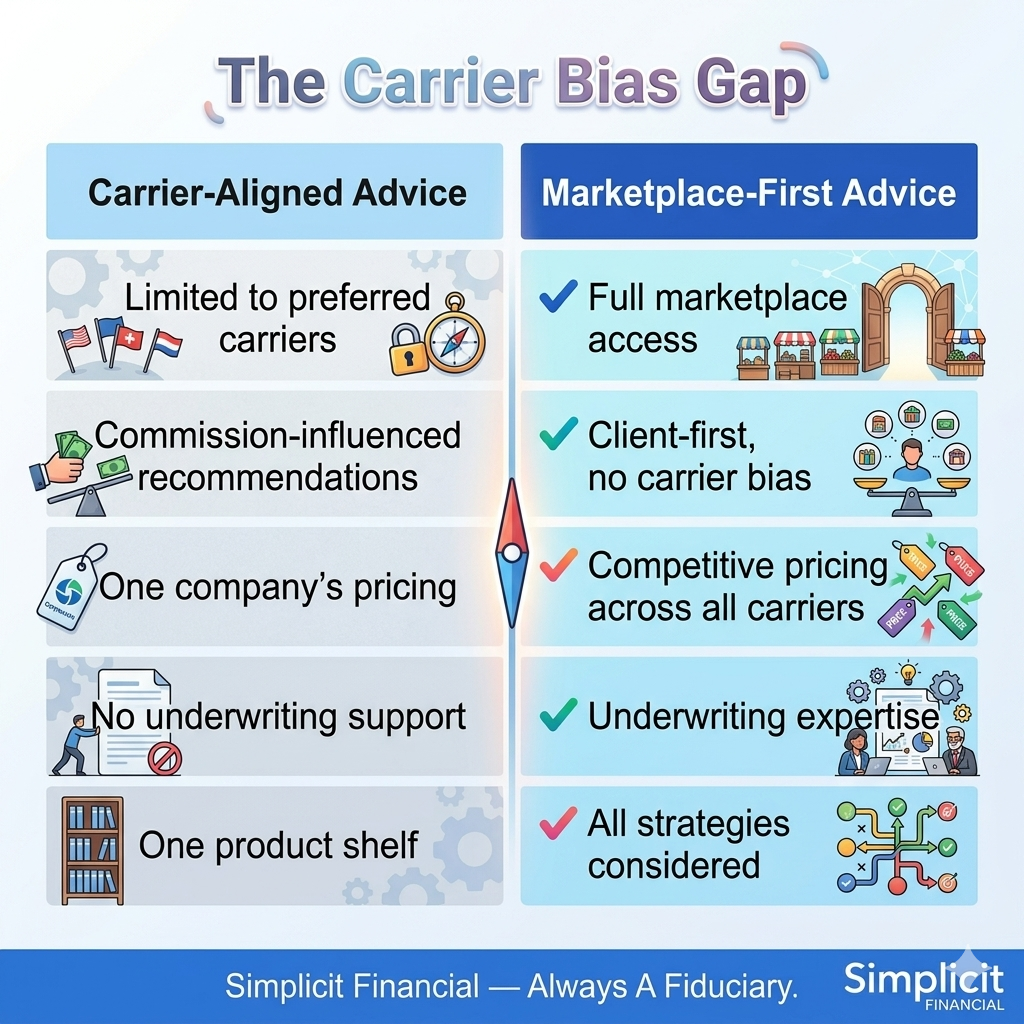

Carrier bias occurs when an insurance professional’s recommendations are influenced — consciously or not — by their relationship with specific insurance carriers rather than by what’s objectively best for the client.

This happens for several structural reasons:

• Captive agents work exclusively for one company and can only offer that company’s products. If a client’s profile doesn’t fit that company’s pricing sweet spot, the options are limited.

• Independent agents often develop preferred carrier relationships over time — based on compensation arrangements, spiffs and relationships. These relationships subtly (and sometimes not so subtly) shape what products they lead with.

• Compensation structures in the insurance industry create incentives to recommend products with higher commissions, longer premium payment periods, or features that benefit the carrier more than the client.

None of this requires bad intent. It’s a structural reality of how the distribution of life insurance has worked for decades. But the result is that many business owners end up with policies that were sold to them rather than designed for them.

What It Costs in Practice

The dollar impact of carrier bias isn’t always visible in the moment — but it shows up over time. Here’s what it can look like for a business owner:

Overpaying on premium

Two business owners with identical health profiles and coverage needs can receive wildly different premium quotes depending on which carrier an agent works with. A carrier that prices unfavorably for a specific age, health condition, or industry can result in premiums that are 20–40% higher than what the market would offer if the full marketplace were accessed.

Underperforming cash value

Universal life and indexed universal life policies are not created equal. Crediting rates, cap rates, participation rates, and fee structures vary significantly by carrier. A policy illustration that looks compelling at point-of-sale can look very different ten years in if the carrier’s product was never the most competitive option for that client’s profile.

Wrong structure for the planning purpose

Whether a policy is structured as term, whole life, universal life, or indexed universal life matters enormously for a business succession or estate planning application. The carrier with the most competitive pricing on term may not be the right carrier for a buy-sell funded with permanent insurance. A carrier-first recommendation can result in a policy that technically provides the death benefit but doesn’t integrate well with the broader plan.

Missed alternatives

A carrier-aligned advisor can only recommend what their carriers offer. That means alternatives like premium-financed strategies, split-dollar arrangements, or life settlement options for existing policies may never come up in the conversation at all — not because they’re wrong for the client, but because they don’t fit the advisor’s product shelf.

What Objective Insurance Advice Actually Looks Like

Objective insurance advice starts with the client’s goals — not with the carrier’s product lineup. Here’s what that process looks like at Simplicit Financial:

Step 1: Understand the planning purpose

Is this policy for buy-sell funding, estate liquidity, key person protection, executive benefits, or supplemental retirement income? Each purpose has different structural requirements that should drive carrier selection — not the other way around.

Step 2: Build the design criteria

Based on the planning purpose, what type of policy, coverage amount, funding timeline, and cash value structure is appropriate? This design is established before any carrier is evaluated.

Step 3: Access the full marketplace

With clear design criteria, we go to the full marketplace — every major carrier — and identify which carriers price most favorably for this specific client’s profile, health history, and planning need.

Step 4: Physician-supported underwriting

Use our 30+ years of underwriting expertise to get the best results for your client. We understand the power of communication with the underwriter. We have a physician who can review the client’s health profile and help position the case for the best possible underwriting classification. This step alone can save a client thousands of dollars annually in premiums — and it’s a capability most insurance professionals simply don’t have.

Step 5: Transparent comparison

We present options across carriers with a clear explanation of the trade-offs — not a single recommendation that serves our interest rather than the client’s.

Why This Matters for Advisors Who Refer Insurance Work

If you’re a financial advisor, estate planning attorney, or CPA who refers clients for insurance placement, the quality of the advice your client receives reflects on your relationship with them. A client who ends up in a policy that underperforms, costs too much, or doesn’t fit their plan is a client who may quietly wonder whether the referral was in their best interest.

Partnering with an insurance specialist who has access to the full marketplace and no carrier bias is a form of due diligence. It’s how you ensure that the insurance piece of your client’s plan is held to the same standard as the rest of it.

Simplicit Financial was built specifically to be that partner — for advisors who want to refer insurance work with confidence that their clients are getting objective, strategy-first recommendations.

The Question Worth Asking

If your clients have existing life insurance policies, the right question isn’t just “Is the premium still being paid?” It’s: “Was this policy ever the right one? And is it still?”

We offer policy reviews that answer both questions honestly — with no incentive to recommend anything other than what’s best for the client.