10 Reasons a Life Settlement May Be the Right Move When a Policy No Longer Fits the Plan

Life insurance is purchased to solve a problem. But problems change. Businesses get sold. Children become financially independent. Estate plans get restructured. Buy-sell agreements get rewritten.

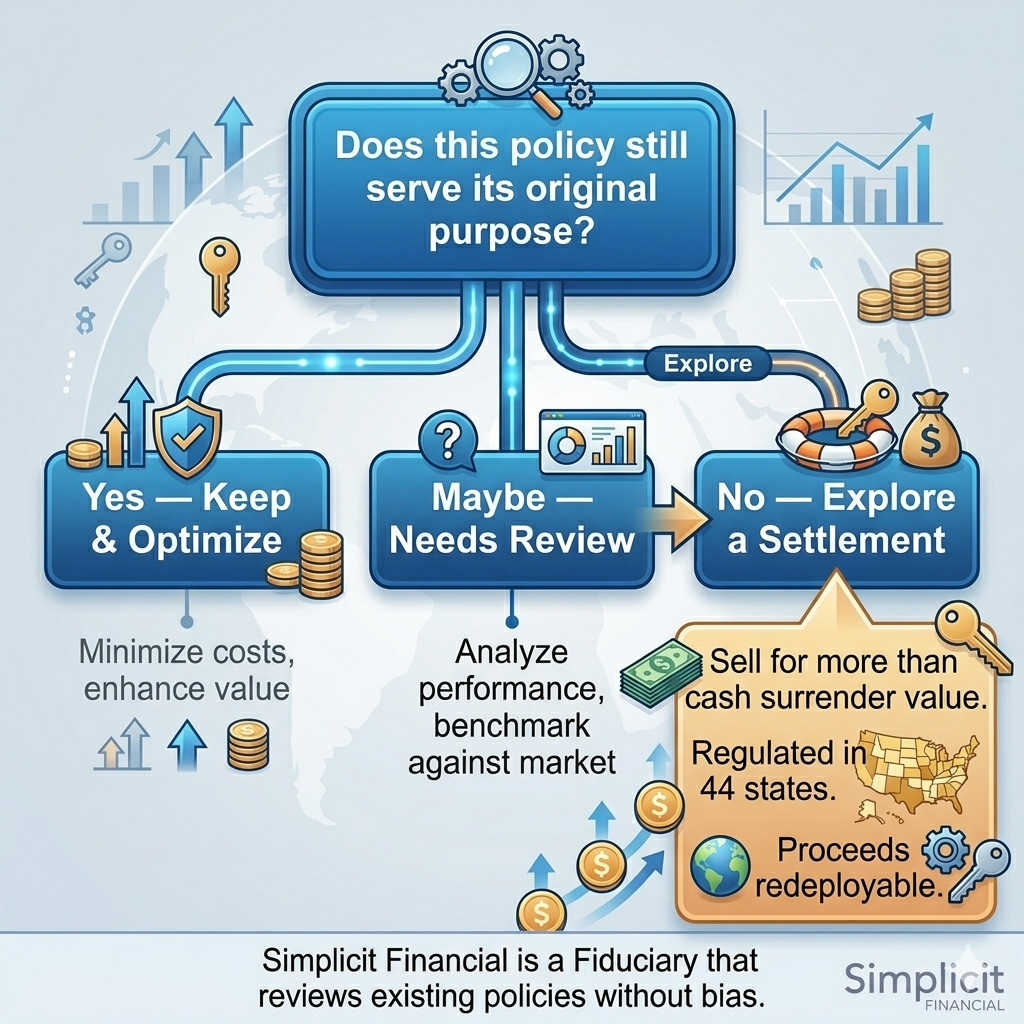

What happens to the policy when the problem it was designed to solve no longer exists?

For many clients, the answer has been: keep paying premiums on a policy that no longer serves its purpose, let it lapse and walk away with nothing, or surrender it for the cash value — which is almost always less than the policy is actually worth.

There is a fourth option that most clients have never been told about: a life settlement.

What Is a Life Settlement?

A life settlement is the sale of an existing life insurance policy to a third-party buyer on the secondary market. The policy owner receives a lump sum payment — more than the cash surrender value, less than the death benefit — and the buyer assumes the premiums and eventually collects the death benefit.

The market is mature, well-regulated, and federally recognized. The U.S. Supreme Court established in 1911 (Grigsby v. Russell) that life insurance is personal property that can be sold. The NCOIL Life Settlement Model Act of 2010 added consumer protections and transparency requirements. Today, life settlement regulations are in place in 44 states and jurisdictions, and institutional investors including banks, pension plans, insurance companies, and private equity firms participate as buyers.

This is not a fringe strategy. It is a planning tool that most clients have simply never been introduced to.

10 Reasons a Life Settlement May Be Worth Exploring

1. The policy no longer fits the estate plan. Estate plans evolve. If the original purpose of the policy — estate liquidity, equalization among heirs, funding an ILIT — has changed, the policy may be worth more to a secondary buyer than it is sitting unused.

2. Premiums have become unaffordable. If a client can no longer sustain the premium burden, lapsing the policy means forfeiting all value. A life settlement captures value before that happens.

3. The death benefit is no longer needed by heirs. When children are financially established or the surviving spouse has sufficient assets, the insurance protection the policy was designed to provide may no longer be necessary.

4. A chronic illness or long-term care need requires liquidity now. A settlement can convert a policy into cash when a client faces unexpected care costs, providing a bridge that other assets may not.

5. The policy is underperforming and projected to lapse. Universal life policies in particular can erode over time if interest crediting assumptions from original illustrations haven’t held. Rather than pour more premiums into a failing policy, a settlement captures what remains.

6. The insured has outlived the original planning purpose. A key person policy on a founder who has since retired. A term policy converted to permanent on an insured who is now 80. The original rationale may have expired even if the policy hasn’t.

7. The business the policy was tied to has been sold. Business sale, liquidation, or dissolution leaves many policies without a purpose. Rather than surrendering for cash value, a settlement typically returns significantly more.

8. The buy-sell agreement it funded has been restructured. Post-Connelly, many business owners are unwinding stock redemption buy-sells and restructuring as cross-purchase agreements. Policies owned by the entity that no longer serve the new structure are candidates for settlement.

9. A 1035 exchange into a more efficient policy is the better long-term path. In some cases, the settlement proceeds are best redeployed into a new, properly structured policy that fits the client’s current situation — rather than continuing to carry a policy built on outdated assumptions.

10. The cash received can be redeployed into a more efficient strategy. Whether that means funding a different insurance strategy, addressing estate liquidity, or simply improving the client’s financial position, the settlement proceeds have value in motion.

What Makes Objective Advice So Important Here

The challenge with life settlements — and with life insurance recommendations generally — is that most advisors who work in this space have a carrier relationship. They earn more when a client keeps a policy in force. They earn more when they replace it with a new one from a preferred carrier. The incentive to recommend a settlement, which benefits the client but generates no new premium revenue, is structurally weak.

At Simplicit Financial, our model is built on objectivity. We have access to the full insurance marketplace with no carrier bias. When we review an existing policy, we evaluate it on its merits — and if the best answer for the client is a life settlement, that’s what we recommend.

We also service policies we did not originally place. If a client brings a policy to us for review, we look at it honestly, regardless of who sold it or how old it is. That kind of objectivity is exactly what clients deserve when they’re making decisions about assets that could be worth tens or hundreds of thousands of dollars.

How to Know if a Life Settlement Conversation Is Warranted

A policy review is the right starting point. If any of these conditions apply to a client, the settlement question is worth asking:

• The policy is more than 10 years old and hasn’t been reviewed

• The insured is over 65 with a policy originally tied to a business purpose

• The business has been sold, restructured, or the buy-sell has changed

• The client is facing premium increases they may not be able to sustain

• The estate plan has changed significantly since the policy was purchased

Simplicit Financial conducts policy reviews that look at both the in-force performance of an existing policy and the strategic question of whether it still belongs in the plan at all. That is the conversation advisors should be having with their clients — and the one most of them aren’t.